Link: Apply for a Bilt credit card, whether you’re a new or existing cardmember

Bilt has announced massive changes, including the introduction of three credit cards in partnership with Cardless, plus an all-new system for being rewarded for rent, which is based on the Bilt Cash currency.

Just about everything about Bilt is changing, for better or worse, and I covered all those details in a previous post. In this post, I’d like to share my personal strategy after having digested all of this information, including the card I decided on, how my application went, and my overall thoughts.

Why I decided to “upgrade” to the Bilt Palladium Card

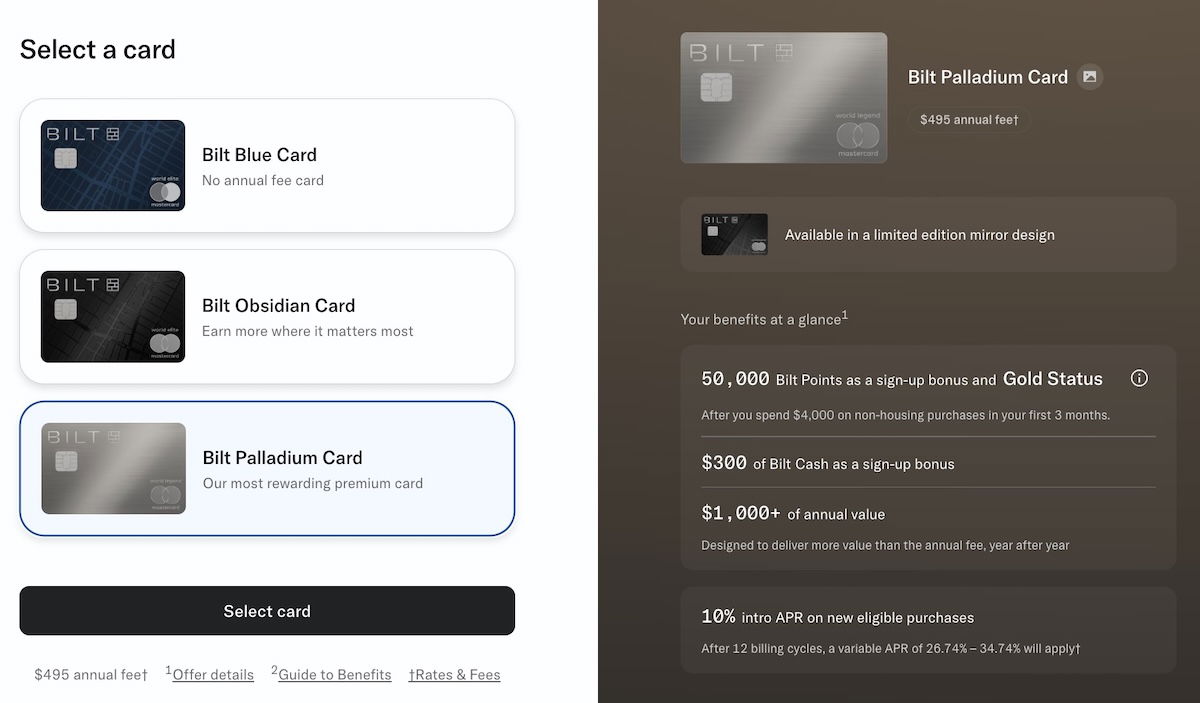

In the previous post, I covered the details of the three new Bilt credit cards, so I don’t want to go over all of that again. Long story short, I think the no annual fee Bilt Blue Card and $95 annual fee Bilt Obsidian Card are sort of non-starters, and it’s hard to get excited about them, especially compared to the old Bilt Card, and especially in comparison to the competitive landscape.

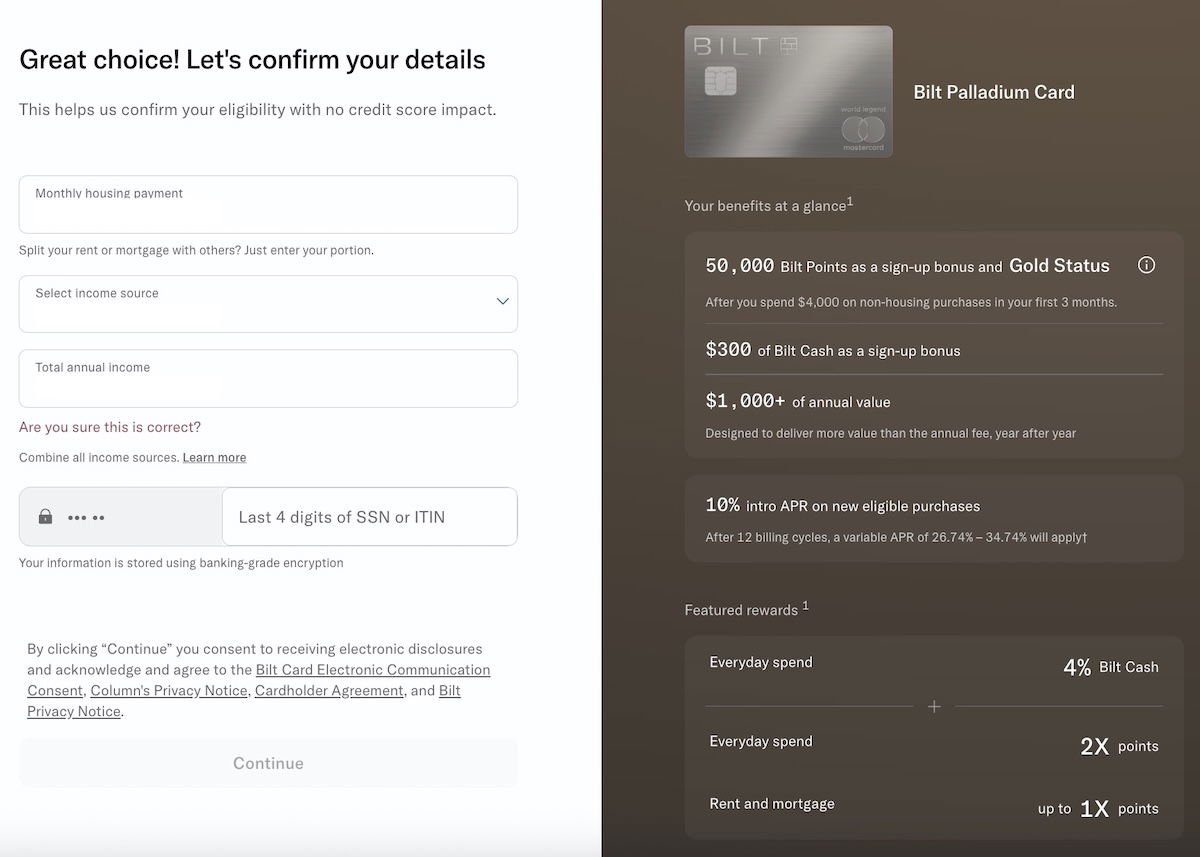

Meanwhile I think the $495 Bilt Palladium Card is the product that’s most worth considering. Why? For one, the card has a welcome bonus of 50,000 bonus points and Bilt Gold status after spending $4,000 within three first three months (on non-housing purchases), plus $300 Bilt Cash upon approval.

We’ve never seen a Bilt card have a formal welcome bonus before, and that’s absolutely worth taking advantage of, as the other two cards don’t offer any points with the bonus. At a minimum, the card is worth giving a try for a year.

Beyond that, what intrigues me about the card is simple — it offers 2x Bilt points on everyday spending, which is pretty incredible. Bilt points are super valuable, as they can be transfered to Alaska Atmos Rewards, World of Hyatt, and a variety of other programs.

While we’ve seen some transferable points cards offer 2x points, I think being able to earn Bilt points at that rate is incredible, and probably beats the other options.

The icing on the cake is that is that you’re earning 4% back in Bilt Cash on all your spending. While there are more questions than answers about alternative uses of Bilt Cash, on the most basic level, you can use that Bilt Cash to pay your rent or mortgage with no fee while earning points.

$3 in Bilt Cash is worth 100 Bilt points on your total rent or mortgage payments, at the rate of 1x points. That’s not exactly straightforward, so just to give an example (on the high side, for easy math), let’s say you spend $100,000 per year on the card:

- You’d earn 200,000 Bilt points, at the rate of 2x points per dollar spent

- You’d unlock the ability to make $133K(ish) in rent or mortgage payments annually on the card, earning 1x points at no fee

- You’d earn Bilt Platinum status, which gives you extra benefits, like some partner status perks, access to better Rent Day offers, etc.

If you spend a decent amount on credit cards, I think it’s hard to beat the combination of earning among the most valuable transferable points at the best rate possible, while that spending also unlocks the ability to earn points on your rent or mortgage.

At a minimum, I think this is worth giving a try, especially with the welcome bonus and easy transition. The challenge will be figuring out how to recoup the $495 annual fee over time. The card does offer a Priority Pass membership, plus up to $400 in Bilt portal hotel credits per year (a $200 credit semi-annually, each requiring a minimum two-night stay).

The restrictions on that hotel credit are potentially a little annoying, but at a minimum, I think the card is worth giving a try for a year. As I see it, there are lots of outstanding questions that haven’t yet been answered, and which will help me decide whether to keep the card beyond the first year:

- Will Bilt keep offering generous Rent Day transfer bonuses to travel partners, which make it a very compelling currency? For that matter, will Bilt keep all of its current transfer partners, and continue to allow points earning with Rakuten?

- Will Bilt let people pay taxes by credit card (for a fee) through other services, or try to add restrictions there, to limit spending? The updated terms suggest that tax payments aren’t considered “eligible purchases,” and I’m curious if that’s enforced, since that would make this one of the few cards that doesn’t reward tax payments

- How will Bilt Cash actually be redeemable beyond offsetting the fee for rent or mortgage payments, since that hasn’t been fully announced?

So yeah, I’m putting this card in the category of absolutely being worth trying, but it remains to be seen if it’s the best option in the long run, based on how things play out. I’m also curious to see how much I actually spend on the card in non-bonused categories, since that will determine how much of the annual fee I’m really recouping. I need to be able to spend a lot — and earn a lot of points — for the $495 annual fee to make sense.

My experience “applying” for the Bilt Palladium Card

As Bilt transitions from Wells Fargo to Cardless, existing cardmembers have the option for a seamless transition. The idea is that you’re supposed to “pre-order” your new card by January 30, 2026, so that you can transition to the product on February 7, 2026, when the card formally launches.

If you’re an existing cardmember, there’s no hard pull when you apply for the new card, and instead, there’s just a soft pull. So unless something absolutely drastic changed since your previous application, you’re supposed to also be approved for the new card. After all, your credit card number will even stay the same as you transition to the new product.

With that in mind, let me share my experience. After going to Bilt’s new credit card page, I logged into my account and clicked the “Apply now” button, and I could choose which card I wanted. I selected the Bilt Palladium Card.

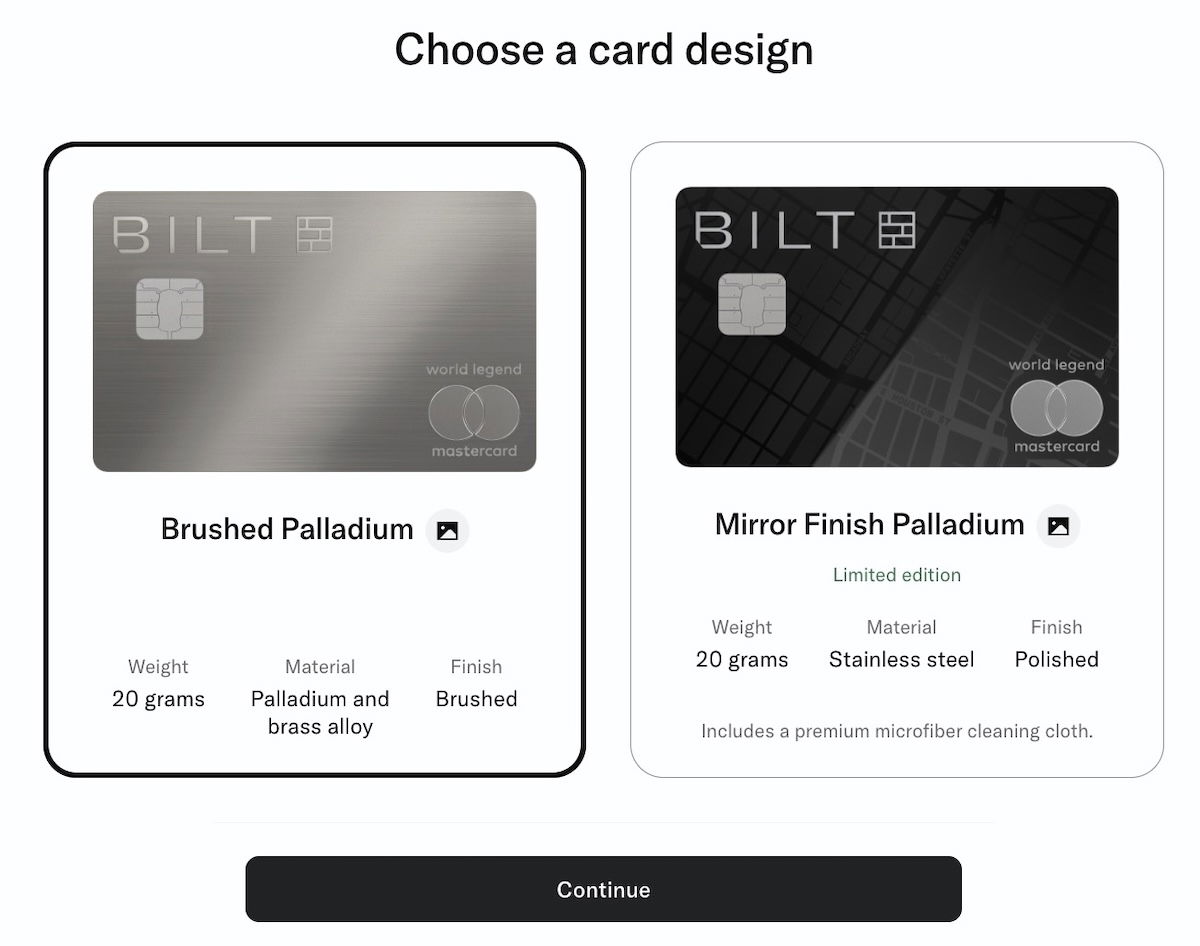

I could then choose my card design, between brushed palladium or mirror finish palladium.

I was then asked to confirm the information I had provided to Wells Fargo in the past, including my monthly housing payment, income, etc.

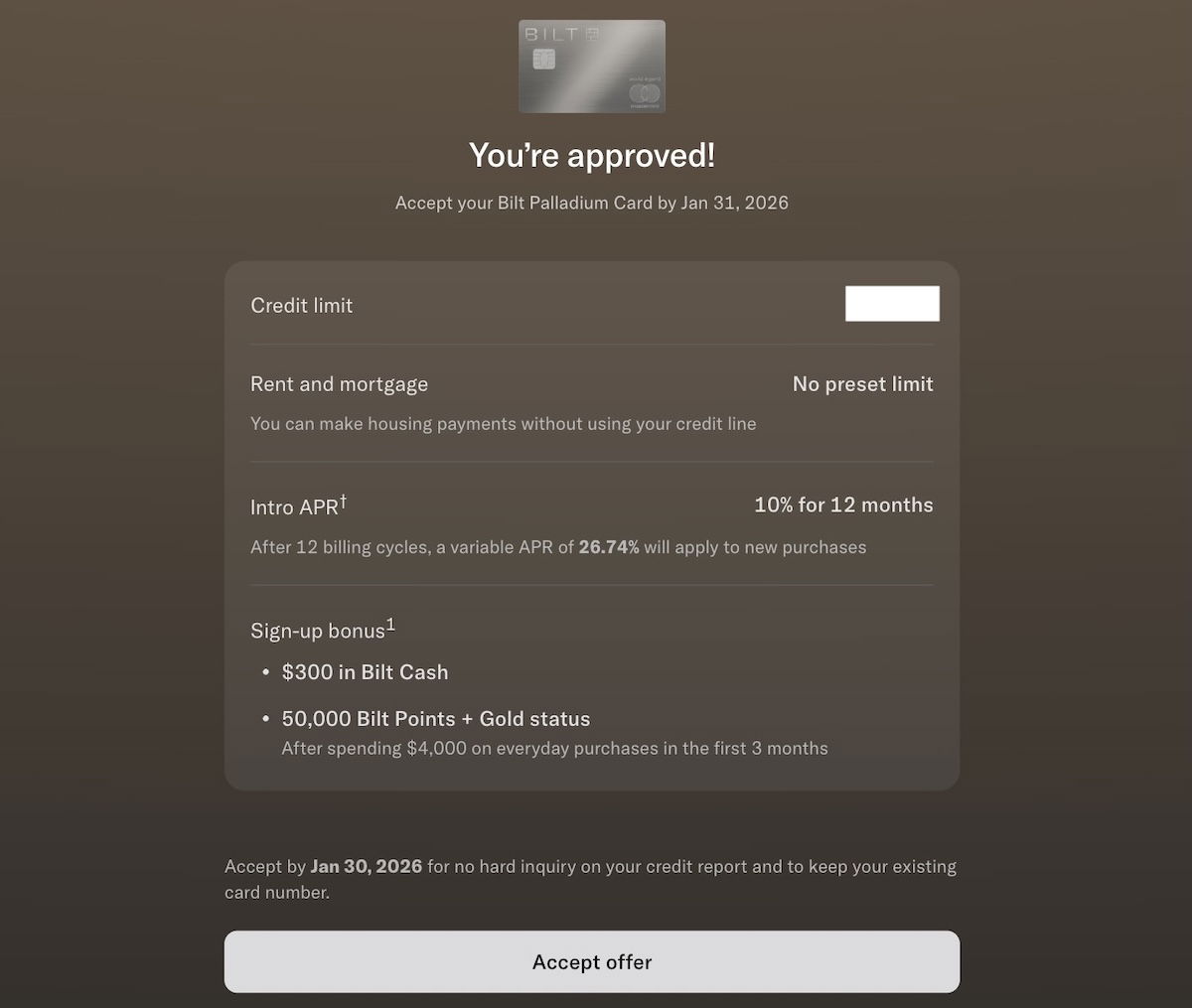

I then submitted that information and found that I was approved, with a big credit line (though it was still about 30% smaller than my Wells Fargo credit line, which was oddly large). Keep in mind that with the transition to Cardless, your rent or mortgage payment no longer counts toward your credit line, so that gives a little more flexibility. I was asked if I wanted to accept the offer.

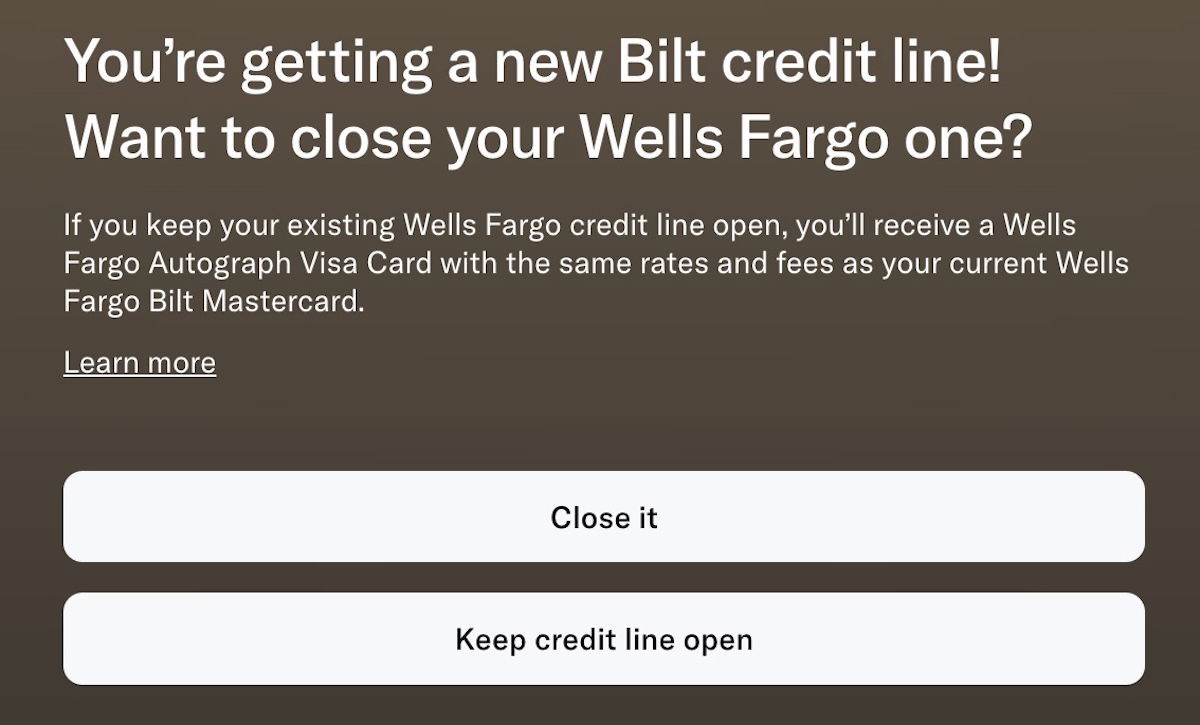

After accepting the offer, I was asked if I wanted to keep my Wells Fargo credit line open, which I didn’t want, so I clicked “Close it.”

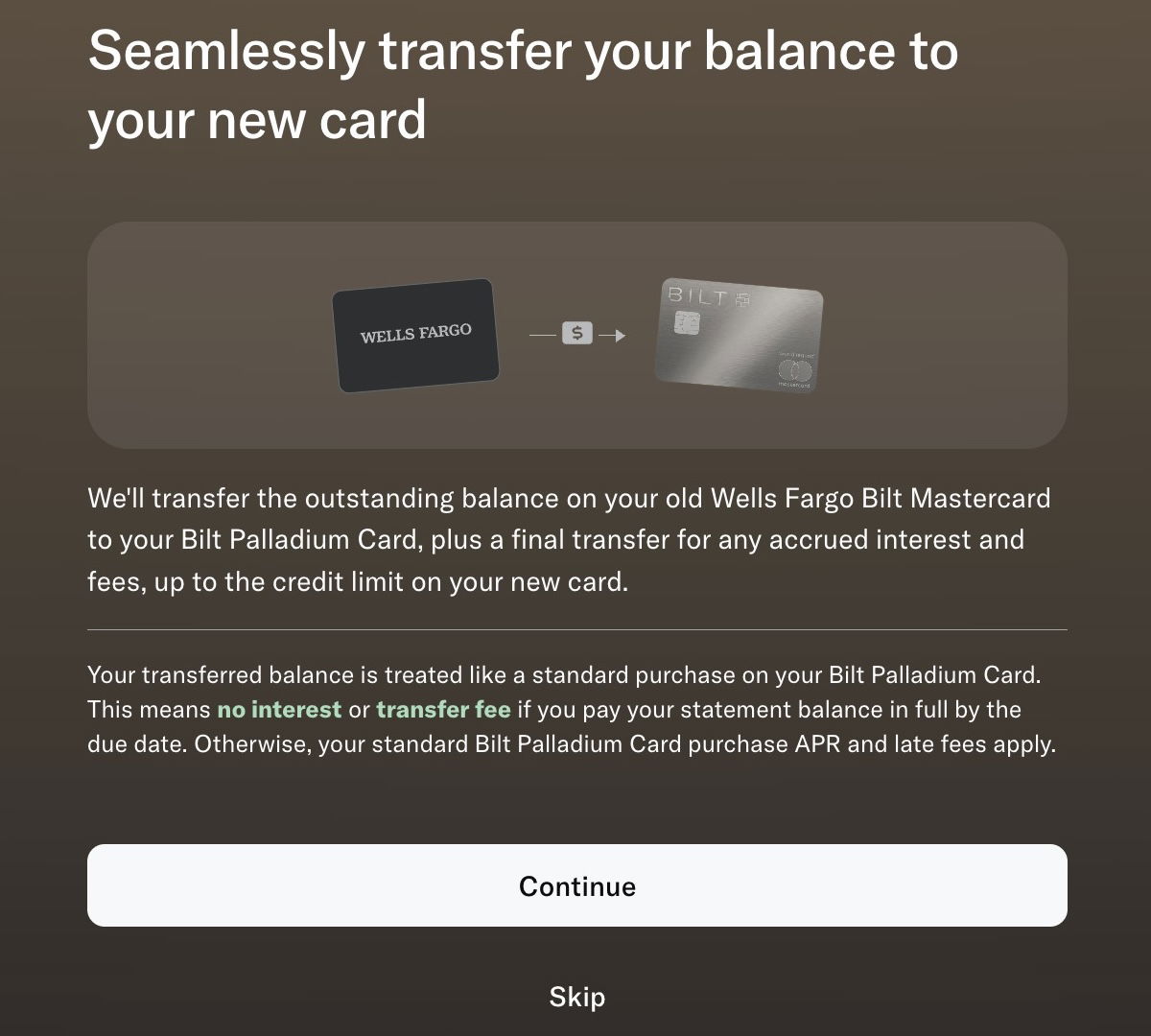

Lastly, I was asked if I wanted to transfer my balance to my new card, and I said that I did.

All-in-all, I found it to be a straightforward process.

Bottom line

We’ve just seen the Bilt credit card portfolio change completely, along with a new system for being rewarded for rent and mortgages. If you are going to continue to be involved in the Bilt ecosystem, then I think the $495 annual fee Bilt Palladium Card is the obvious choice, assuming you spend a decent amount on your credit card, and on rent or mortgages.

It’s the only card with a substantial welcome bonus, and as I view it, that bonus more than covers the card’s annual fee for the first year. The biggest selling point of the card is that it earns 2x points on all spending, which I’d argue makes it one of the best cards out there for everyday spending, given the value of Bilt points.

However, there are a few unknowns here, so for now I’m simply viewing this as a card that I’m giving a try for a year, and then I’ll decide on my long term strategy based on how things play out.

How are you thinking about which Bilt card makes the most sense, and which did you decide on, if any?

Link da fonte