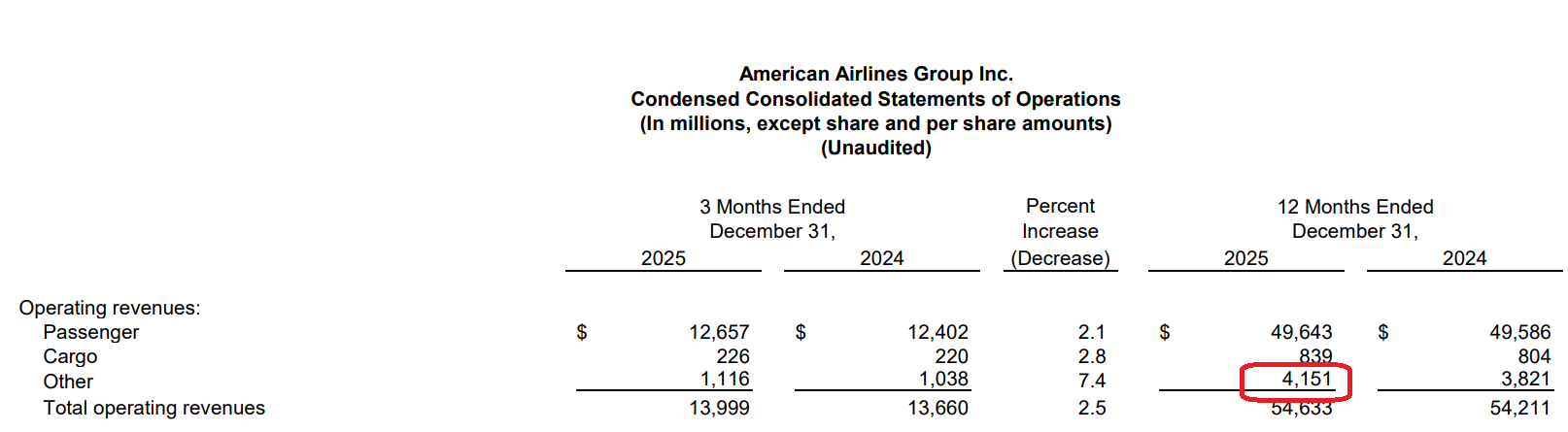

For the full year, American Airlines earned just $111 million on $54.6 billion revenue. That’s a one quarter of one percent margin. Basically break-even.

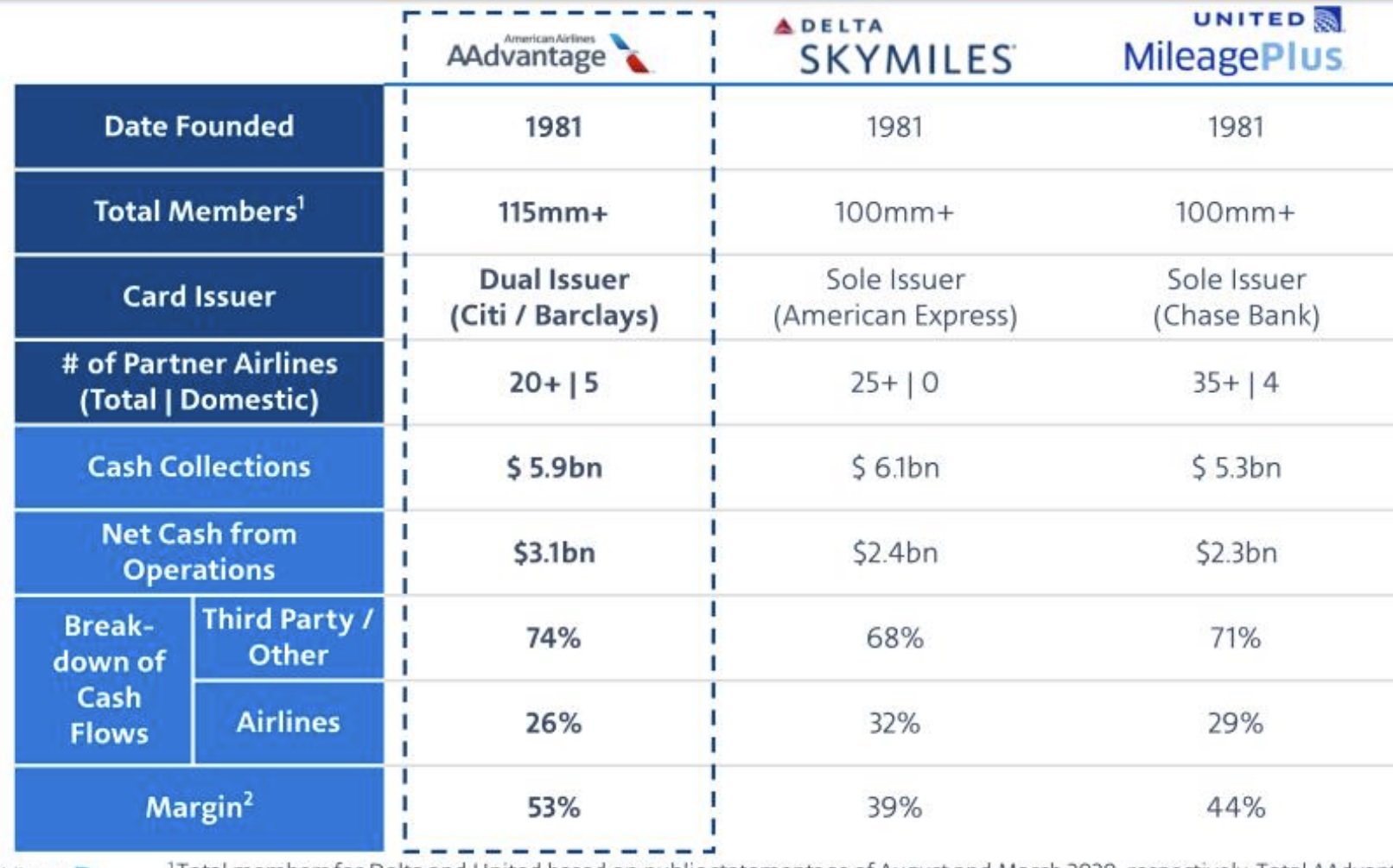

- American has previously reported a 53% margin on American AAdvantage, which is thus roughly driving $2 billion in profit. Actually flying planes is losing about $2 billion.

- It’s hard to get to exact numbers on this, airlines do not disclose a lot of detail on their programs and each does the internal accounting differently (American’s program probably doesn’t actually operate at a one-third higher margin’s than Delta’s). But it gives us an order of magnitude. They aren’t really making money on the miles ‘sold’ internally for flying, or sold to partner airlines. It’s the banks. For back of the envelope, just look at other income.

- You wouldn’t want to shut down the airline and just sell AAdvantage miles to Citibank. Nobody would want them. In fact, the more American flies in a market the more relevant they are to customers and that’ll drive greater spend on their Citi products.

- Nonetheless, it’s clear that American has been offering the wrong airline product, chasing the wrong customer, for the past dozen years.

They are trying to change this, with better reliability and a better product. That takes huge investment and takes time.

At its core, American has been:

- Flying to the wrong markets. American’s Sun Belt strategy has been worthwhile, but not at the expense of top cities. American has lost its position in key markets – New York, Chicago, Los Angeles (where they have hubs) and the Bay Area and Pacific Northwest where they’ve never been especially strong. But that’s where the most consumer spending is. They make their money on credit card business, and charge volume on their card product has gone from number one amongst airlines to number three.

- Lacking the right aircraft. American hasn’t had the planes to build back in these markets. They retired too many during the pandemic, including widebodies that could have allowed them to take advantage of the boom in Europe travel and higher profit opportunities in Asia with Chinese carriers no longer offering as much capacity.

- Pivoting away from premium at the exact wrong time. They focused on competing with Spirit and Frontier, walking away from product investment right as customers were looking for more premium options. They added seats to planes, taking premium seats out and adding coach with less space and few extra legroom seats as well.

Operationally, they’ve not just failed to meet Delta and others in on-time reliability, they’ve lost more wheelchairs and mishandled more bags and they’ve been unwilling to make investments like RFID tracking (as Delta does) because it’s too expensive. There hasn’t been enough line maintenance, either.

They’ve been adding premium seats, and – recognizing that most passengers actually fly coach, coach passengers are also premium passengers on long flights and are tomorrow’s prmeium passengers – they’ve been adding modestly to food for sale on board. And they’ve added free wifi, matching Delta and JetBlue and the direction United and Alaska are heading (and Southwest offers, with poor wifi). And they’re investing in the operations of their DFW hub.

If they’re willing to make the big investments – in new planes, in clubs, in food – and if the top leaders of the airline are willing to sell a vision to customers and especially to employees out at their stations – then a several years-long effort could turn the airline around. Without profits, though, it’s unclear how much runway they’ll have to make the investments.

And until we see the capital expenses and the CEO on the road with employees, we won’t know how committed the airline is to this kind of turnaround.

More From View from the Wing

Link da fonte