In the miles & points world, we’re rather obsessed with maximizing value, and scoff at the thought of not redeeming our points for multiple cents each. That almost always comes in the form of travel redemptions, typically by moving points to airline partners, often for premium cabin redemptions.

However, I think sometimes we forget the extent to which we’re not average consumers…

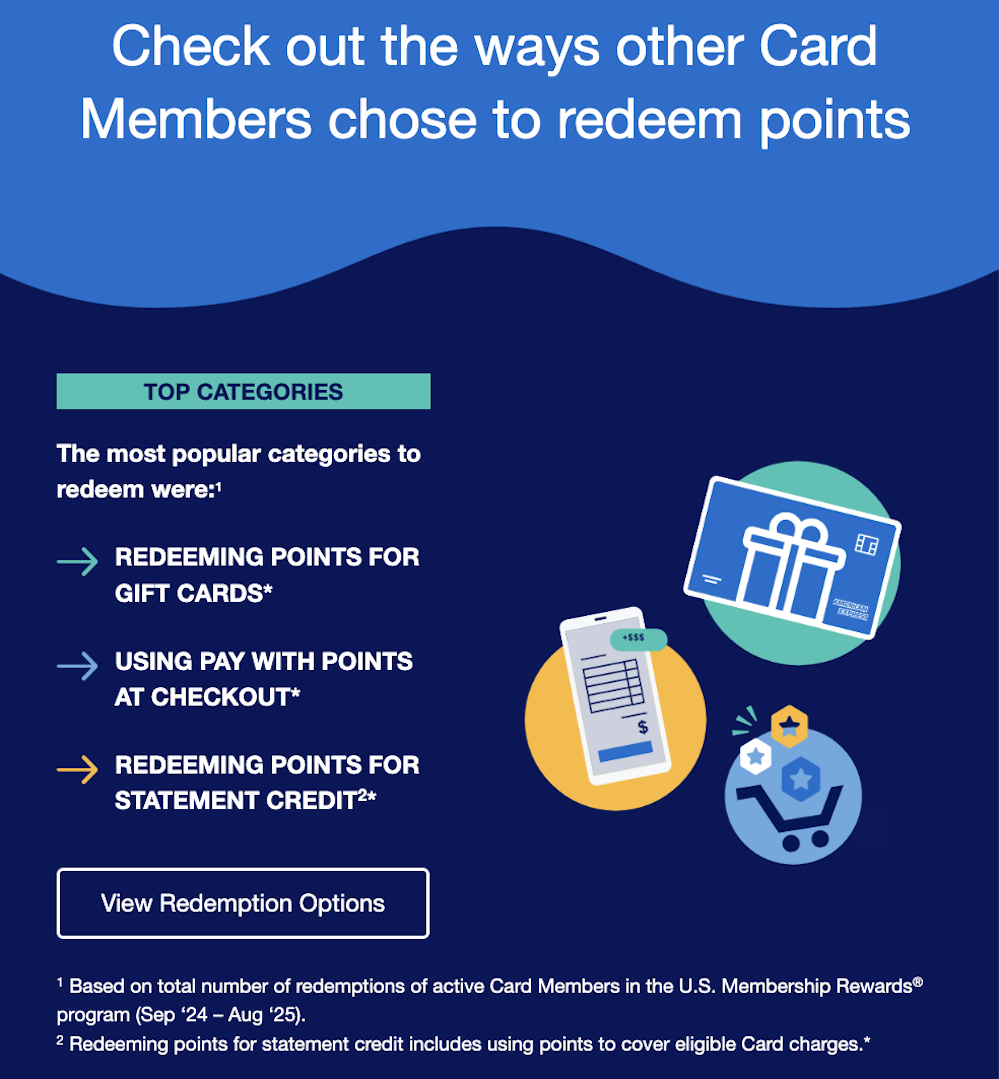

Amex reveals the way that members redeem points

OMAAT reader Jack sent me the following email, along with the below screenshot.

Amex sent me this “Points Pulse: year in review” email today, and I found this part fascinating. I know that points optimizers are a minority, but somewhat surprising that points transfers don’t even crack the top 3? I don’t think they’d lie given how specific they are in the footnote. I wonder if the order is accurate – surprising to see gift cards as #1 – maybe they’re just trying to push people in that direction. Amazing for AmEx that all three of the most popular options cost them less than one cent per point. Can’t help but think of Bilt who are competing against this and have customers who are way more likely to transfer points (usually with massive bonuses).

Personally, I value Amex Membership Rewards points at 1.7 cents each, and that’s thanks to the ability to get outsized value by moving the points to transfer partners, and then redeeming for first and business class travel.

For what it’s worth, all three of these redemption options — gift cards, paying with points at check-out, and statement credits — get you a fixed 0.6-0.7 cents of value per point.

This is what makes credit card economics fascinating

Credit card issuers make money through several means, including interchange fees, annual fees, and financing charges.

What’s interesting is that when you move your Amex points to an airline or hotel partner, it’s potentially actually quite costly for them. There’s no set pricing across the board, since all currencies are worth different amounts, but we have reason to believe card issuers are paying around 1.5 cents per point for some currencies.

So to me, it’s a fascinating twist to credit card economics. The major banks are of course very profitable, but they’re certainly not making money on all customers, and certainly not equally. Quite to the contrary, many “maximizers” might not actually be that profitable, due to how they redeem their points.

All else being equal, card issuers would of course rather that you’re redeeming your points for 0.6 cents of value, rather than something that might be costing them more than double as much. It’s just wild that some people are basically earning back the entire interchange fee in the form of credit card rewards (and sometimes even more), while others are earning back maybe well under one-third of the typical interchange fee.

To me, this is also all such a reflection of how sub-optimally people use credit cards, and how they might choose a card issuer based on name or reputation. But if your goal is to simply earn cash back (which is what all of these popular redemption options are, more or less), there are very rewarding cash back cards in the market that can earn you a minimum of 2% back.

Bottom line

Amex has revealed the top ways that members redeem points, and they include gift cards, paying with points, and statement credits. These redemptions get you an average of 0.6-0.7 cents of value per point, which is a fraction of the value that many of us try to get with our Amex points. For that matter, it’s also a fraction of how much many travel redemptions cost Amex.

It’s a good reminder of the extent to which those of us optimizing our points are the minority, and how most people aren’t actually very savvy about the card they choose (because if you wanted to earn cash back, you can do much better than a 0.6-0.7% rate of return).

Are you surprised by these Amex points redemption details?

Link da fonte